Updated: June 29, 2019

Overview

All Separately Managed Accounts (SMA) are currently being migrated to a new custodian (Interactive Brokers1), which requires your action. Please follow the instructions below to activate a Euro Pacific Trader account so we can continue with your managed account migration.

Why? What is Euro Pacific Trader?

When we opened your managed account, we first opened a standard Global TradeStation (GTS) brokerage account, and then signed a management agreement. In April, we decided to end our relationship with Saxo Bank, who offers the Global TradeStation brokerage account, and are now replacing them with Interactive Brokers1 and the new platform, called Euro Pacific Trader (EPT).

How will this affect me?

From your perspective, very little will change:

- As usual, you will not have trading access to your managed account

- However, we will need to send you a new View-Only portal for you to view your account at the end of July

- Our new custodian (Interactive Brokers1), has much cheaper trading commissions, more products, and more exchanges, which will help us greatly in the management of your assets

- You’ll keep the same portfolio structure, strategies, and fund managers (Euro Pacific Advisors)

Your next steps

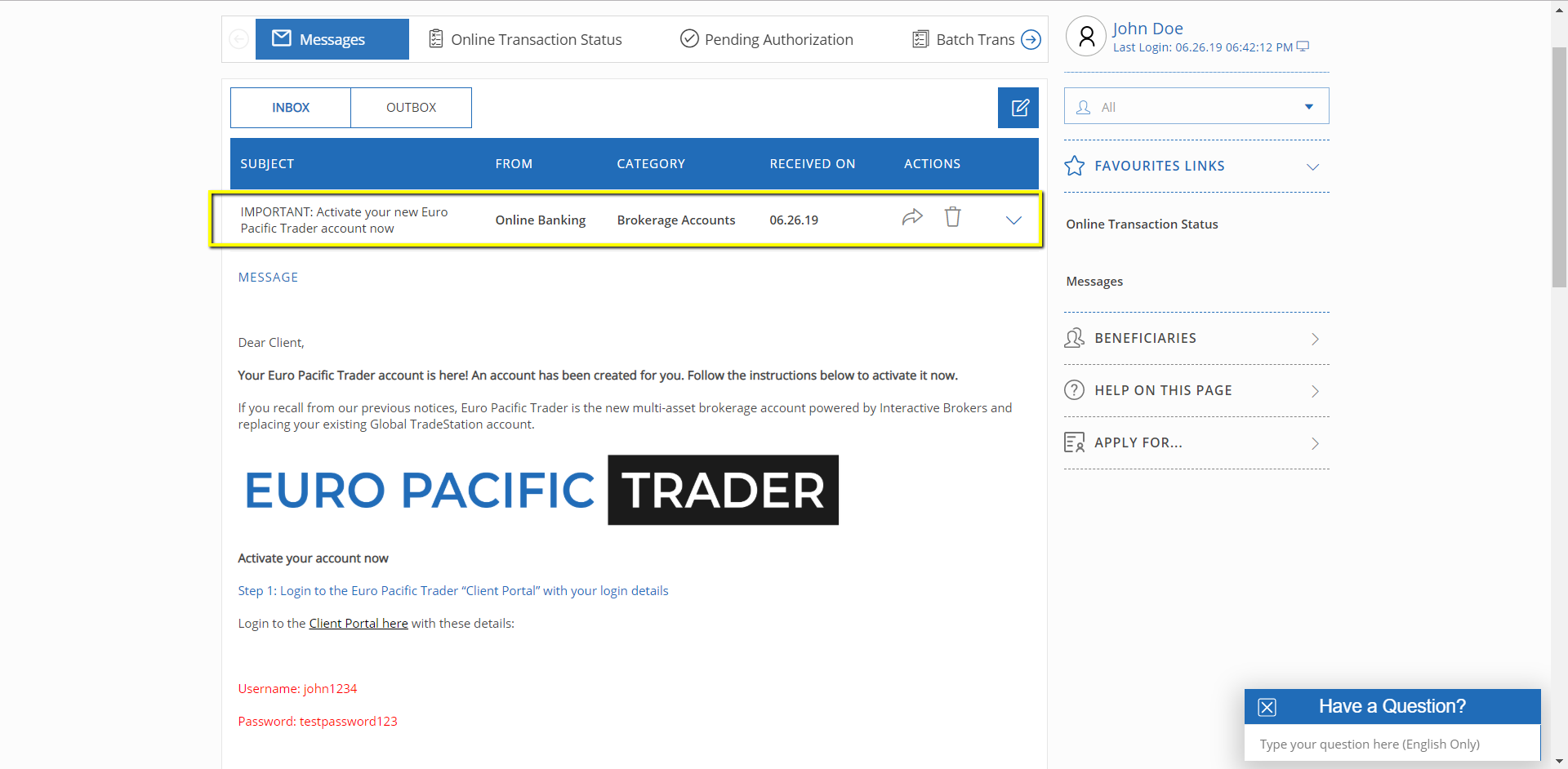

1. Login to your eBanking

Read our recent secure message with the subject line IMPORTANT: Activate your new Euro Pacific Trader account now.

Haven’t received the secure message?

1. We are still sending out secure messages this week, so it’s possible we haven’t sent you one yet. If this is the case, please email [email protected] and request your login credentials.

2. We may also be trying to contact you to gather missing information or documentation on your account. Please check your recent secure messages for any unread mail.

2. Log into your EPT Client Portal

After logging into your EPT Client Portal for the first time, you will be asked to complete a short, electronic compliance form. This information will be used to process US Source Income every year, a mandatory regulatory requirement.

Note: Some clients may be required to fulfill outstanding document such as a W8 or CRS Form or may be requested additional documentation like a new, scanned proof of address, in order to keep our records up to date.

3. Check your account activation status

If you have logged into your Client Portal successfully and submitted your compliance form, the EPT account will be activated within 4-5 business days, unless more information or documentation is required. To check your Account Activation Status, simply log into your Client Portal again.

If your account is activated, you will arrive at your Client Portal home page successfully.

If you have any questions about where you are in the activation process after you have submitted the compliance form, please send us an eBanking secure message or email [email protected] and we will reply confirming the status of your Euro Pacific Trader account.

4. Migrating your stocks

Starting July 1st, equity positions for clients with activated Euro Pacific Trader accounts will be migrated. This will occur gradually over the period of July 1-19th.

Update: A majority of positions were successfully allocated by August 9th. Some positions have not been allocated due to settlement delays between Saxo Bank and Interactive Brokers, however these remaining positions will be allocated throughout August.

5. View your account

Please note that your existing managed account view-only Client Portal will be discontinued at the end of July and replaced with a new one. We will be issuing you a new view-only portal at the end of July. If you need any managed account statements in the meantime, please let us know.

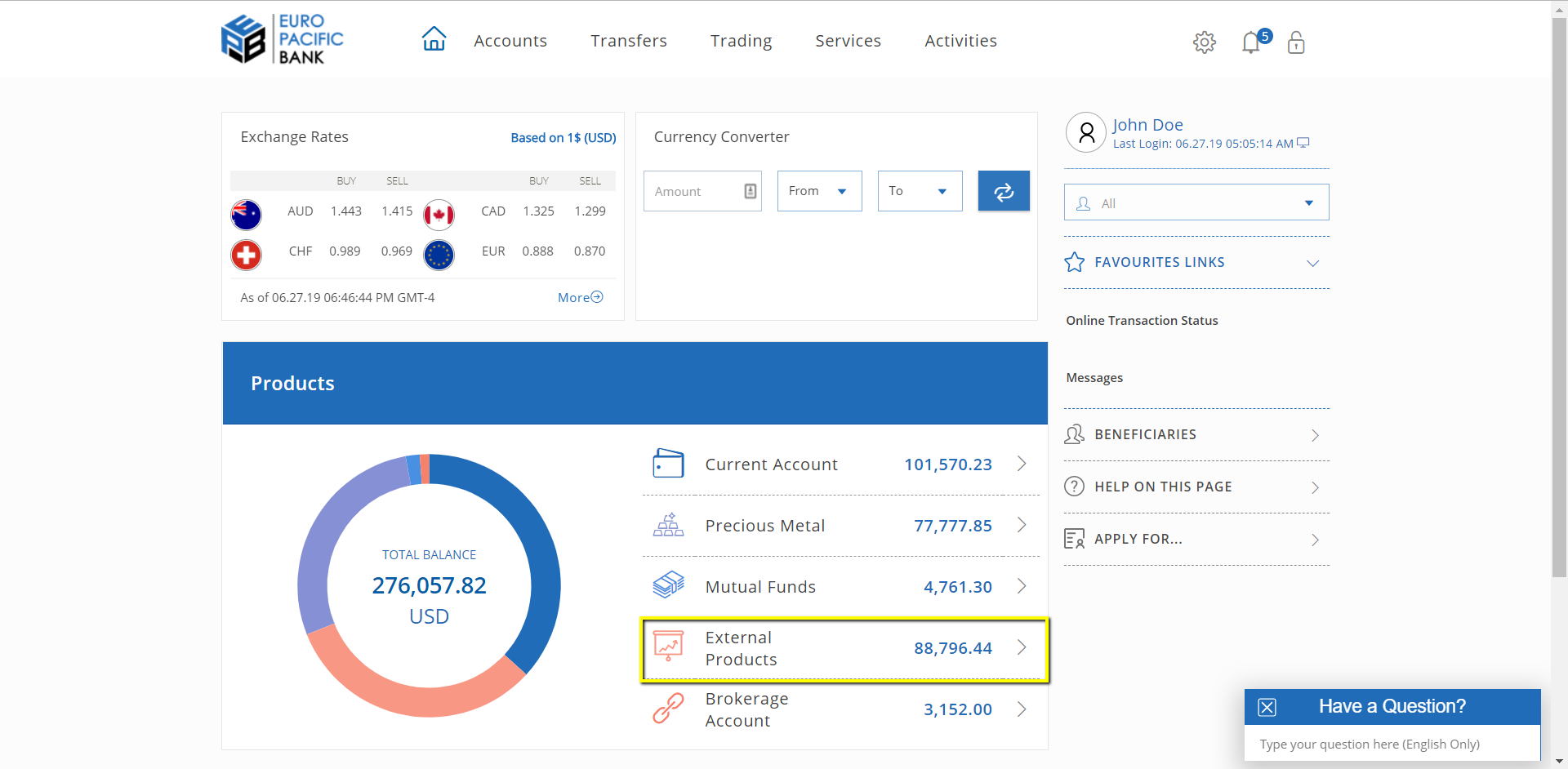

Second, due to the migration, your eBanking dashboard’s External Products section will not reflect an accurate balance at this time, but we do intend to re-launch this feature in the near future.

1Disclaimers:

Euro Pacific Trader is offered by Euro Pacific Securities Inc. (“Euro Pacific Securities”), as an Introducing Broker to Interactive Brokers LLC. Interactive Brokers LLC is the custodian, technology provider, and clearing broker to all transactions executed through Euro Pacific Trader and thus the rates, conditions, and examples shown on this site may be subject to change and differ from what is displayed on Euro Pacific Trader. The rates, conditions, and examples on this site are provided on a best-efforts basis and should not be taken as final.

Euro Pacific Securities will not be held responsible for pricing and conditional discrepancies that may arise in the normal course of offering Euro Pacific Trader. Customers should always review and rely on the conditions that are shown directly on Euro Pacific Trader, and it is the responsibility of all customers to carefully review the conditions of every action before approving execution on Euro Pacific Trader.

Interactive Brokers LLC is a registered Broker-Dealer, Futures Commission Merchant and Forex Dealer Member, regulated by the U.S. Securities and Exchange Commission (SEC), the Commodity Futures Trading Commission (CFTC) and the National Futures Association (NFA), and is a member of the Financial Industry Regulatory Authority (FINRA) and several other self-regulatory organizations. Interactive Brokers LLC does not endorse or recommend any introducing brokers, third-party financial advisors or hedge funds, including Euro Pacific Securities. Interactive Brokers LLC provides execution and clearing services to customers. None of the information contained herein constitutes a recommendation, offer, or solicitation of an offer by Interactive Brokers LLC to buy, sell or hold any security, financial product or instrument or to engage in any specific investment strategy. Interactive Brokers LLC makes no representation, and assumes no liability to the accuracy or completeness of the information provided on this website.For more information regarding Interactive Brokers, please visit www.interactivebrokers.com.